Business Credit Cards That Pull TransUnion Only

Author: Dylan Buckley

January 22, 2026

7 min read

TABLE OF CONTENTS

- 1. Business Credit Cards That Pull TransUnion Only

- 2. The BMO Business Platinum Card

- 3. The Bank of America Business Advantage Card

- 4. The U.S. Bank Business Platinum Card

- 5. What To Do If You Only Have Good Credit With One of the Credit Bureaus

- 6. Can You Get a Business Credit Card without Personal Credit?

- 7. Build Business Credit to Qualify for Better Cards

- 8. Fund Your Business and Grow Your Business Credit With FairFigure

Start your credit building journey for your business

Most business credit cards will perform a personal credit check. It can be advantageous to leverage your best credit scores when applying for a business credit card.

If TransUnion features your best score, here are a few business credit cards that pull TransUnion only.

Business Credit Cards That Pull TransUnion Only

The BMO Business Platinum Card

The BMO Business Platinum Rewards Credit Card is a solid choice for those who like rewards.

The BMO Business Platinum Rewards Credit Card features no annual fee, 0% introductory APR for the first nine months, and added discounts and perks like cell phone coverage and tax filing discounts.

This BMO business credit card uses a points system. You earn:

- 5x points on every $1 you spend on internet and phone services

- 4x points on office supplies and printing

- 3x points on gas stations and EV charging stations

- 2x points on eligible dining purchases

- Unlimited 1x points on all other eligible purchases

They also offer bonus points if you meet spending thresholds in the specified window of time. At the time of writing, this looks like a bonus of 50,000 points if you spend $5,000 in three months. If you spend $50,000 in 12 months, you can get an additional 50,000 points.

These rewards don’t expire.

The standard variable APR for this business credit card ranges from 19.49% - 28.49%. This is a little high, but great if you can land the lower rates.

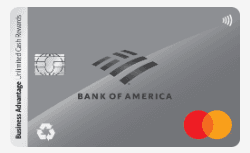

The Bank of America Business Advantage Card

Are you looking for a lower variable APR and a non-points-based business credit card? If so, you might consider the Business Advantage Unlimited Cash Rewards Mastercard Credit Card.

The Business Advantage Unlimited Cash Rewards Mastercard Credit Card is a hassle-free card.

You get 1.5% cash back on all purchases. There’s no annual cap, and rewards don’t expire.

You can boost this to unlimited 2.62% cash back. However, this is only possible if you have a qualifying business checking account with Bank of America.

They offer an online statement credit of $300 if you spend $3,000 within 90 days of account opening.

Their rates are a bit better than BMO’s. Like BMO, they don’t have an annual fee. They offer a 0% introductory APR offer for the first nine billing cycles. After that, you’ll have a variable APR of anywhere from 17.49% to 27.49%.

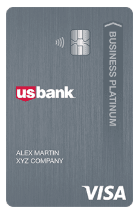

The U.S. Bank Business Platinum Card

The U.S. Bank Business Platinum Card is the best credit card here if you enjoy lower variable APR and longer 0% APR introductory periods.

The one downside is the lack of rewards. Unlike the above options, there are no rewards with the U.S. Bank Business Platinum Card.

You do receive some benefits. These include dedicated service, seamless card management, and the ability to use U.S. Bank ExtendPay Plans.

Unlike the previous choices, you won’t have to deal with interest for a longer period of time. They offer a 0% APR introductory offer for 12 months. Your card also comes with no annual fee.

Variable APR will range from 16.99% to 25.99% depending on creditworthiness.

What To Do If You Only Have Good Credit With One of the Credit Bureaus

It’s not uncommon for scores to vary across personal credit bureaus. Variations in how consumer credit bureaus calculate scores and the information they’ve received mean that one score might look slightly different than the other.

But it’s still worth questioning.

In some cases, your score could be higher with one bureau due to errors. Request your free personal credit report and look for:

- False credit information that is impacting your credit report. These could be errors or signs of potential identity theft.

- Missing transactions.

- Incorrect account balances, which can increase your reported credit utilization.

- Wrong payment dates.

- Closed accounts that haven’t been reported as closed. Sometimes, a credit bureau may accidentally add an account back after reporting it as closed.

- Accounts that have been duplicated.

Take care to review each personal credit score regularly and dispute where needed.

If it’s not a matter of incorrect information in your personal credit report, you’ll just need to make sure you’re following credit-building best practices to see higher scores across the board. Until then, you’ll need to focus on options like secured business credit cards that report to D&B.

Can You Get a Business Credit Card without Personal Credit?

Relying on one good score to land you a business credit card might not be the best strategy. But what most business owners don’t know is that you don’t have to rely on personal credit to get a business credit card.

One way to circumvent personal credit checks is with EIN-only cards. EIN-only cards consider a myriad of factors (revenue, time in business, etc.) and only rely on your business credit. Credit decisions won’t be made based on your personal credit.

Most traditional financial institutions, like banks, don’t offer EIN-only cards. You’d have to generate millions in revenue and be established to circumvent personal credit checks.

But many small businesses can turn to solutions like charge cards, fleet cards, and unique EIN only business credit card solutions, like FairFigure.

Keep in mind that some business credit cards can affect your personal credit. Research which business credit cards do not report personal credit to keep your credit safe.

Build Business Credit to Qualify for Better Cards

Building business credit opens up a whole world of funding opportunities to you.

It’s similar to what you’re able to achieve with personal credit. If your personal credit score is low, you won’t be able to access much aside from a secured credit card. If your scores are great and you’re a responsible person, you can tap into so much more.

It’s important to build business credit so you can qualify for better cards. This will land you lower interest rates, more lucrative perks, and a higher initial credit limit.

But where do you begin?

Fund Your Business and Grow Your Business Credit With FairFigure

FairFigure makes it easy for small business owners to grow their business credit.

The first solution we offer is our business credit monitoring service. Priced at just $30/month, this service is reported to more than one business credit bureau.

This helps you build credit while keeping an eye on your business credit scores from each of the major credit bureaus.

With your subscription comes access to the FairFigure Capital Card. The FairFigure Capital Card is an EIN-only business credit builder card.

We report to Dun & Bradstreet, the Small Business Financial Exchange (SBFE), Equifax, CreditSafe, and our Foundation Report.

This will allow you to build your business credit score and credit history efficiently with an additional tradeline.

It doesn’t require a personal guarantee. It also doesn’t require paperwork to apply.

If you make $2,500 a month or more and have been in business for at least three months, you can qualify for this card. It’s not a charge card, and you get to choose your payback terms (4 or 8 weeks).

Sign up for FairFigure today to fund your small business and build business credit!

More articles

Read More >

July 20, 2026

7 min read

July 09, 2026

8 min read

July 09, 2026

2 min read

Start your credit building journey for your business

Start your credit journey now with FairFigure