How Hard Is It to Get a Business Loan?

Author: Dylan Buckley

January 23, 2026

9 min read

TABLE OF CONTENTS

Start your credit building journey for your business

How hard it is to get a business loan depends entirely on the type of loan you’re looking to get, and the requirements of the lender.

We look at easy business loans and hard business loans to help you understand what your options are for your small business.

Easy Business Loans

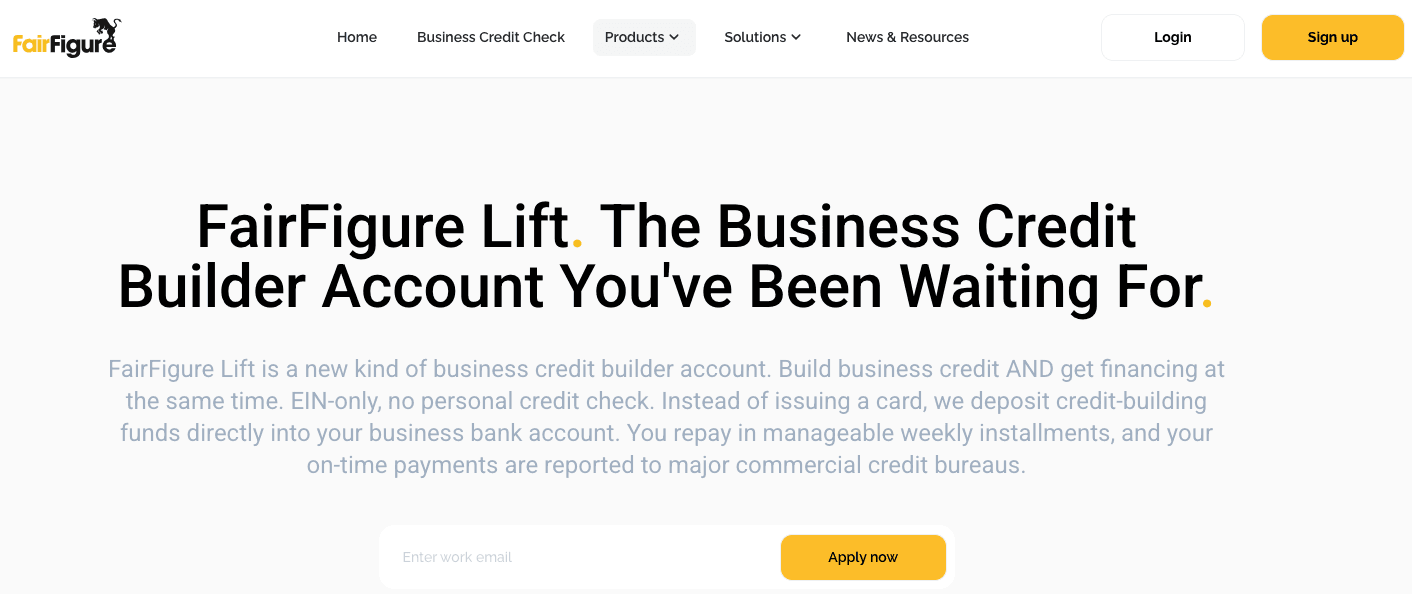

1. FairFigure Lift

If you need to build business credit and finance your business, you could always turn to FairFigure Lift instead of a traditional business credit card.

FairFigure Lift is a new kind of EIN-only business credit builder account. No personal credit score or credit history is needed.

You get funds deposited directly to your business bank account, make payments weekly over the course of four to eight weeks, and build credit over time.

All payments are reported to Equifax, Experian, Creditsafe, and the SBFE. Unlike a business credit card, you also receive two tradelines to boost your business credit score: this business credit builder account and your FairFigure business credit monitoring account.

2. Credit Cards

Business credit cards help you finance your business by giving you a revolving line of credit that you can draw from regularly to manage business expenses and help you boost your cash flow.

The best credit cards you will qualify for most easily include corporate cards and fleet cards. These business credit card solutions consider annual revenue and equity investment instead of personal credit scores and credit history.

You can get a secured credit card if you have poor personal credit scores and credit history. However, these solutions come with high fees and interest rates. A secured loan is a similar loan option that might be a better fit for the average small business owner.

3. Merchant Cash Advance

A merchant cash advance (MCA) is a form of small business financing in which you receive a lump sum in exchange for some of your future credit or debit card sales.

Businesses that need fast funding, make a considerable amount in daily credit and debit card sales, and have cash flow needs that they need to solve right away are often best suited for an MCA.

Many MCA providers will check your personal credit score. However, it’s generally a soft inquiry. Your personal credit score also won’t carry as much weight as it does with less obtainable financing solutions.

MCAs are characterized by:

- Factor rates rather than interest rates. For example, if you have a 1.5 factor rate on a $10,000 cash advance, you’d be paying back $15,000 altogether.

- Less stringent qualification requirements that make it easy for businesses turned away from other funding options to get approved.

- Flexible repayment terms that take into consideration your sales.

MCAs do come with some downsides. They can be expensive, require daily payments, and typically require a personal guarantee.

Assess every financing option before springing for an MCA first.

4. Invoice Financing

Invoice financing enables your small business to leverage unpaid invoices in order to access financing.

You approach an invoice lender, receive cash for invoices that you can leverage (not all invoices are eligible), and pay the amount you borrowed back, minus interest and/or fees that the invoice financing lender charges.

Invoice financing can be a quick way to fund your business when other options are unavailable. It’s easy to obtain, and you won’t have to worry about collateral since your outstanding invoices are the collateral.

Invoice financing also doesn’t consider your personal credit score.

Bad credit doesn’t matter for this type of business financing.

`That’s because your personal credit score or credit history doesn’t matter since you’re not the borrower. Instead, invoice financing generally requires a good credit score from each business owner behind the invoice. They will need better than bad credit.

However, it does come with its downsides.

Namely, invoice financing comes with the inherent risk of your customers not paying. The longer your customer doesn’t pay, the more expensive it becomes to use this method.

5. Equipment Financing

Do you operate a specific type of business, like a restaurant, and lack the funding you need to invest in equipment?

Equipment financing is a lump-sum loan that is given to you so that you can purchase equipment for your business.

This type of business loan is easy to qualify for and gives you the ability to own your equipment rather than leasing it. Your equipment serves as collateral for your loan.

If you have a low credit score, equipment financing is a viable solution. A lender won’t be looking too much into your credit score because the equipment you’re borrowing is collateral.

There’s the obvious downside of equipment repossession if you default. However, the true danger lies in the length of the business loan.

Let’s imagine that you manage to secure an equipment loan that you’ve agreed to repay over seven years. At some point during those seven years, your equipment decides to break down.

You’re still on the hook for the business loan when you choose the wrong loan term.

Knowing how long equipment lasts and what equipment financing terms to ask for will help you avoid paying back this business loan long after the equipment has broken down.

6. Car Loans

Businesses that offer delivery, logistical services, or services throughout their locale will need to invest in a vehicle(s) that will support business operations.

Car loans can help you finance these vehicles to get your business off the ground.

Car loans aren’t necessarily easy to qualify for across the board.

However, like consumer auto loans, there are options out there that are going to be designed for business owners with lower business credit and personal credit scores than a traditional lender might demand.

When approaching commercial car loans, always consider:

- How much of a down payment you can/are willing to put down on your vehicle if you need this type of business loan.

- What your options are, getting estimates from more than one lender so you can receive the best terms for your business loan even if you have bad credit.

- Whether you need one car or multiple vehicles. You might need a different type of business loan, like a commercial fleet loan.

- What you’re going to do after you secure your loan. Creating a plan for vehicle trade-in and fleet management will eliminate future problems.

Hard Business Loans

1. SBA Loans

Not looking to work with an alternative lender? Small Business Administration loans are among the best loans for small businesses to secure.

An SBA loan guarantees you lower interest rates, flexible repayment terms, and support from the Small Business Administration should you default on your loan.

SBA loans often require several years in business, high credit scores (at least 690, typically), and strong annual revenue to pay off your loan amount. It’s not the average startup business loan you might qualify for.

The SBA loan approval process can take a while. Getting a small business loan from an SBA lender is not a quick business funding option like many of the financing solutions and loans listed above.

SBA loans are something you should strive for. As a small business loan, an SBA loan is designed specifically around your needs.

However, the reality is that you will need to make sure you meet their strict eligibility requirements and use many of the other solutions above before you will qualify.

When you do qualify, look for an SBA preferred lender offering small business loans. This type of lender can expedite the review and approval process. Not every SBA lender can do this.

The SBA also offers business loans for immigrants, although this type of small business loan is often subject to the same rules as its other offerings.

2. Bank Term Loans

Bank term loans are often accompanied by lower interest rates, longer repayment terms, and a higher loan amount that enable you to invest heavily in your business.

However, like SBA loans, bank term loans are often more difficult to acquire. Banks want to protect their investment, and your credit report and business health will matter.

To do so, they require businesses to have strong annual revenue, good cash flow, an established credit history, and high business credit scores to get a term loan.

You’ll have to work your way up to bank term loans, but it’ll be worth it once they’re accessible to you.

A business credit builder loan might be the right choice for your small business at this point in time if you don’t have a good credit score and need to build business credit. Then, once you’ve built it, you can get a term loan more easily.

3. Bank Lines of Credit

A term loan has its uses, but so do other financing solutions, like lines of credit. Beyond a traditional bank loan, you’ll want to take advantage of business lines of credit.

With a business line of credit, you get access to credit that is continually at your disposal for the duration of our agreement. Take what you want, pay it back, and then tap into it again. This can offer cash flow benefits in comparison to a lump-sum loan amount.

Bank lines of credit have the same eligibility requirements as the other hard business loans listed in this guide.

This can make it difficult for newer businesses to qualify until they’re more established, having the revenue and business credit needed for banks to seriously consider them.

The Takeaway

Many business loans or business financing solutions are easy to qualify for, but the best are typically inaccessible until you are able to meet certain eligibility requirements.

Easy business loans give you the support you need now. Still, focus on building business credit so that you can tap into funding with better terms faster.

More articles

Read More >

July 09, 2026

8 min read

July 09, 2026

2 min read

July 09, 2026

11 min read

Start your credit building journey for your business

Start your credit journey now with FairFigure