Small Business Lending Statistics

Author: Dylan Buckley

July 09, 2026

8 min read

TABLE OF CONTENTS

- 1. Key Takeaways of Small Business Lending Statistics

- 2. Typical Small Business Loan Approval Rates

- 3. Average Business Bank Loan Sizes

- 4. How Much Debt Do Small Businesses Normally Have?

- 5. How Much Revolving Credit Do Small Businesses Normally Use?

- 6. How Often Do Small Businesses Default on Debt?

- 7. How Much Are Average Small Business Debt Charge-Offs?

Start your credit building journey for your business

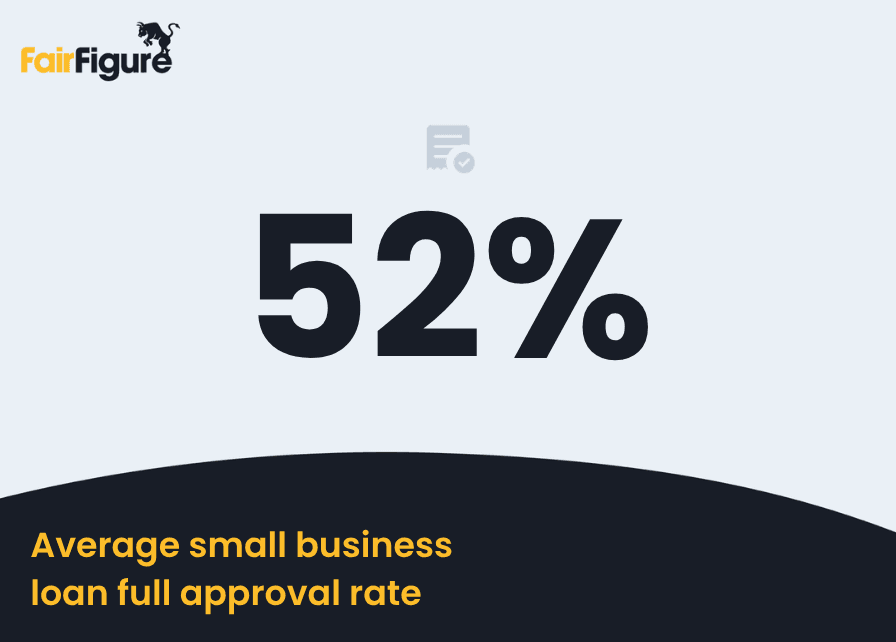

52% of small businesses were approved for small business loans in 2025.

The average business bank loan size sought by small businesses was around $80,000.

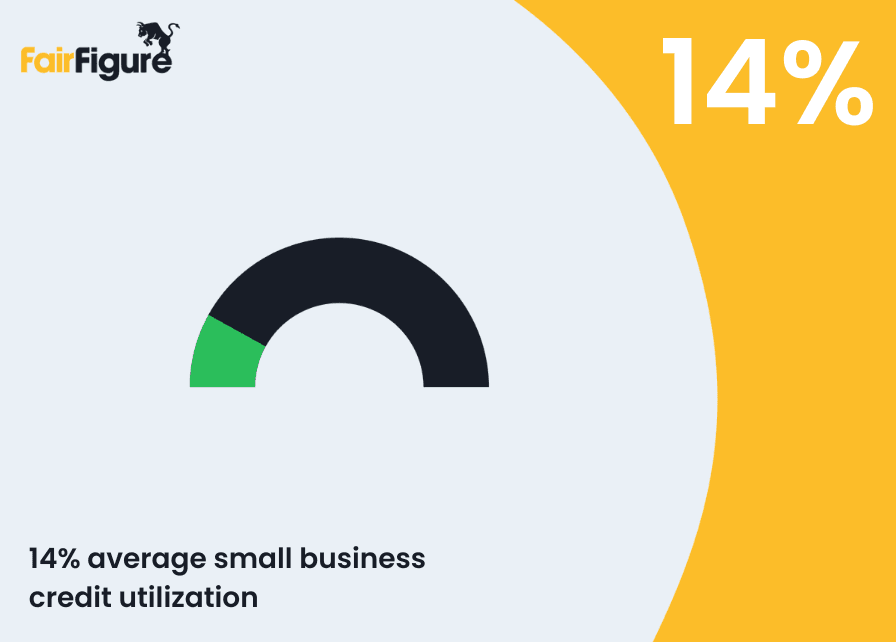

The average small business is using 14% of its available business credit.

We look at the small business lending statistics that illustrate small business financing activity and business credit health.

Key Takeaways of Small Business Lending Statistics

- 52% of small businesses were approved for small business loans in 2025.

- 29% of firms were partially approved, and 19% of firms were denied.

- Small banks had the highest approval rates at 57%.

- The average business bank loan size sought by small businesses was around $80,000.

- The average outstanding debt for small businesses carrying a balance is $14,358.

- The average small business is using 14% of its available business credit.

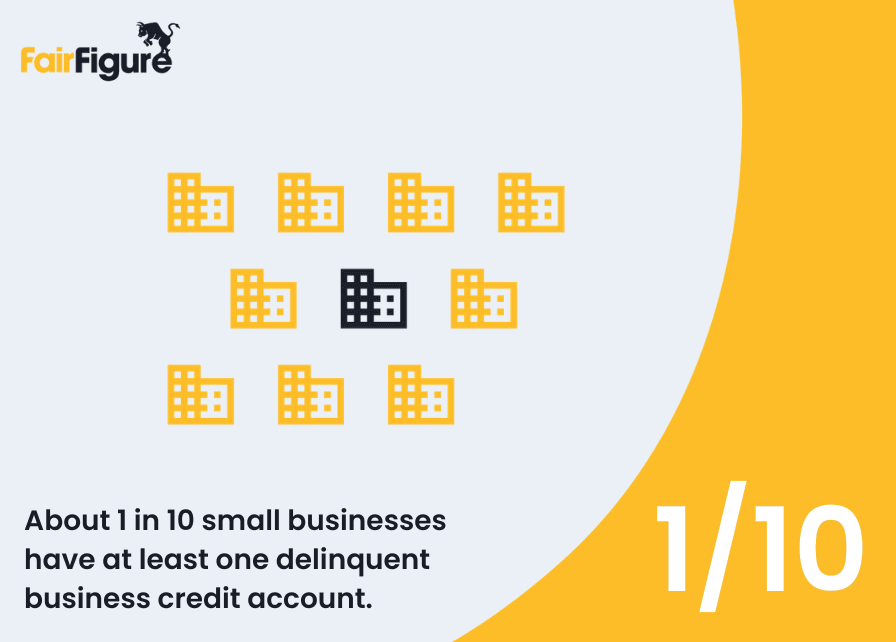

- Approximately 1 in 10 small businesses had at least one delinquent business credit account in 2025.

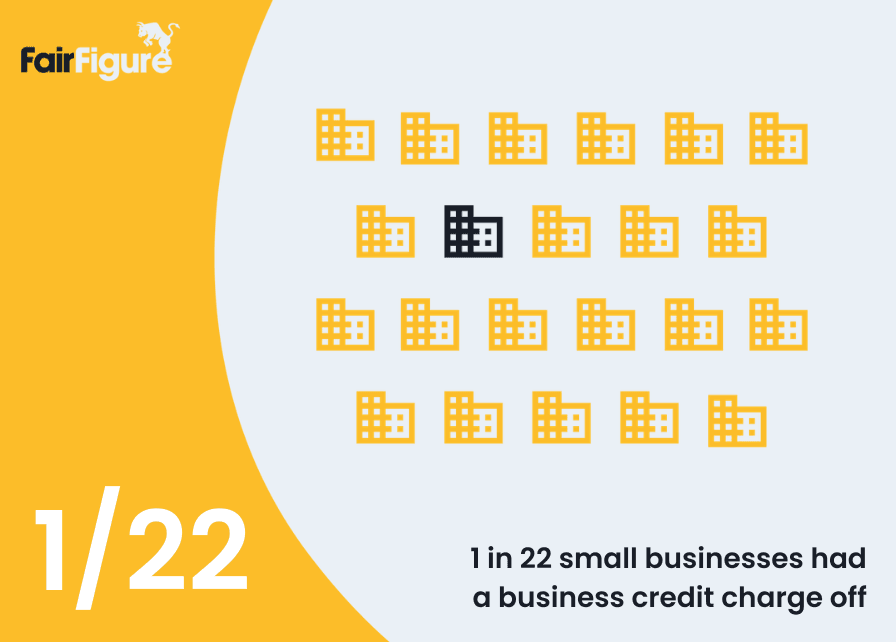

- Around 1 in 22 small businesses had a business credit charge-off.

Typical Small Business Loan Approval Rates

The 2026 Report on Employer Firms from Fed Small Business revealed that 52% of small businesses were approved for loans, lines of credit, or merchant cash advances in 2025.

Meanwhile, 29% were only partially approved, and 19% of applicants were denied.

Those who applied for an auto or equipment loan fared best. 71% of applicants were approved for their loan.

The small business lending survey of small firms also revealed these small business lending statistics surrounding approval:

- 55% of small businesses were approved for a mortgage.

- 48% of small businesses were approved for a merchant cash advance.

- 45% of firms were approved for a business line of credit.

- 40% were approved for a personal loan. (A small business owner should use EIN only business funding instead of a personal loan. This will help you protect your personal credit score and personal finances.)

- 37% of firms were approved for a small business loan.

- 35% of firms were approved for a home equity line of credit.

- 32% of firms were approved for a Small Business Administration loan (SBA loan)/line of credit.

It’s also important to understand where loan approval rates are highest. Small business lending statistics show where applicants are most likely to receive financing.

Applicants at small banks saw the highest rates of full approval at 57%. Finance companies fully approved 50% of applicants.

Meanwhile, credit unions and large banks saw nearly the same loan approval rates at 44% and 43%, respectively. Online lenders had slightly lower approval rates than commercial banks at 38%.

Community Development Financial Institutions (CDFIs) had the lowest approval rate at 27%.

Additional small business lending statistics include:

- Most small businesses applied for a business line of credit. 43% of firms pursued this small business financing solution. 32% applied for a small business loan, and 20% applied for an SBA loan or line of credit.

- Most borrowers sought small business financing at large banks. However, the number approaching online lenders has increased since last year, jumping from 24% to 29%.

- Medium and high-risk credit applicants were more likely to apply for financing with online lenders. 49% applied at an online lender or fintech lender. Meanwhile, only 34% applied at a large bank, and only 21% with medium or high credit risk applied at a small bank.

- Small businesses that applied for large or small bank lending chose their lender based on existing relationships. Those who chose online lenders prioritized speed and likelihood of funding when making their lender decision.

Average Business Bank Loan Sizes

The average business bank loan size sought by small businesses sits at around $80,000. Many businesses sought lower small business loans on average.

The 2026 Report on Employer Firms from the Fed Small Business breaks down these small business lending statistics as follows:

- 21% of borrowers sought around $25,000 or less in funding.

- 16% of small business owners sought $25,000 to $50,000 in funding.

- 22% sought $50,000 to $100,000 in funding.

- 19% sought $100,000 to $250,000 in funding.

- 14% sought $250,000 to $1 million in funding.

- Only 8% of small business owners sought $1 million or more in financing.

Small business lending statistics show us that applications are spread fairly evenly across business credit tiers or types.

Most small businesses (38%) wanted a loan, line of credit, or merchant cash advance. 29% applied for credit cards. 17% sought trade credit, while 11% sought a lease. Meanwhile, only 3% sought factoring.

Fed Small Business also provides us with overall approval rates. 42% of applicants received all of the funding they sought. 15% received most of it, 21% received some of it, and 22% received none of their requested funding.

Of the 22% of small businesses that were not approved, small business loan statistics reveal:

- 46% said that their loan application was not approved because the -lender's requirements were too strict.

- 37% of prospective borrowers were carrying too much debt already.

- 30% had a credit score that was too low for financing approval.

- 29% had insufficient collateral.

- 29% of small enterprises had weak sales.

- 29% stated that the reason was, “Lenders do not approve financing for businesses like mine.”

Note: _While credit denial and refusal to accept some of the funding were two factors that affected approval rates for those who did not receive all of the financing sought, 13% still had applications pending at the time of the survey. _

_67% were not approved, and 37% did not accept some or all of the approved financing.

Small business lending statistics for approval rates may be different as a result of these pending applications. _

How Much Debt Do Small Businesses Normally Have?

External small business lending statistics can be useful. However, we have internal data that can paint a picture of business financial health as well.

FairFigure’s latest small business credit report data reveals that the average outstanding debt for small businesses carrying a balance is $14,358.

Looking at our data, we can also see that the median debt among businesses carrying a balance was $32,669.

Even though this number has more than doubled, it’s important to note that the median balance being carried was much smaller, sitting at $322.

How Much Revolving Credit Do Small Businesses Normally Use?

FairFigure’s latest small business credit report data reveals that the average small business is using 14% of its available revolving business credit.

This is sufficient not only to maintain good credit but to build better credit (especially after getting started with options like a business credit builder loan).

However, don’t let these numbers fool you. There are clear underlying stress signals buried in the data, with 3.5% of businesses utilizing over 80% of their available credit. Meanwhile, 2.7% have already maxed out their available credit.

This means that, among businesses actively carrying balances, nearly 1 in 13 of those businesses is already utilizing more than 80% of their available credit.

How Often Do Small Businesses Default on Debt?

FairFigure’s latest small business credit report data shows us that approximately 1 in 10 small businesses had at least one delinquent business credit account.

When looking specifically at businesses with active reported tradelines, this number rises. Among all businesses with tradelines, 1 in 4 had at least one delinquent business credit account.

This demonstrates that credit stress is most concentrated among small business owners already using business credit.

To further break this down, 6.2% of active business credit tradelines were tied to a delinquent business, while 18.3% of reported trade balances were past due.

Here’s a clearer look at small business delinquency using the available data.

| Delinquency | Percentage of All Businesses | Percentage of Businesses With Tradelines |

|---|---|---|

| Any Delinquency | 9.6% | 25.5% |

| 30+ Days Past Due | 7.4% | 19.7% |

| 60+ Days Past Due | 6.5% | 17.2% |

| 90+ Days Past Due | 4.5% | 11.8% |

How Much Are Average Small Business Debt Charge-Offs?

Per FairFigure’s small business credit report data, around 1 in 22 small businesses had a business credit charge-off. These small businesses had an average severe balance of $8,462.

Charge-offs demonstrate the severe delinquency of some small business owners. The average amount indicates the amount of debt these small businesses are carrying, but are unable to manage before lenders write off their account as a loss.

These small business lending statistics were calculated using business credit reports from FairFigure’s database of 25,000 small businesses with under 10 employees in 2025.

More articles

Read More >July 09, 2026

8 min read

July 09, 2026

2 min read

July 09, 2026

11 min read

Start your credit building journey for your business

Start your credit journey now with FairFigure